Structure for the current market scenario:

Structures that can be bought cheap in today’s market scenario are the ones which are - Short correlation (Realized correlation has been very high in the past one year in the financial markets as compared to the years of bull run), short volatility/structure having minimum Vega exposure since implied volatilities are at an all time high & more bumps are being given to volatility since in strenuous times realized volatility is greater than implied volatility, short skew – Banks are generally short skew & it’s hard to hedge skew for underlying’s which don’t have a liquid option market & long dividends - banks are generally long dividends.

Market Observations:

- Volatility term structure is inverted due to peaking short term volatilities. This implies that forward volatility would be much cheaper now.

- Downside skew for the SPX has come off sharply in recent weeks and is in contrast with the still elevated levels for skew at the single stock level. This is perhaps more consistent with the very high corporate default rates being priced in for both the high grade and high yield credit markets. Similarly emerging market underlying’s are continuing to trade at a high skew.

- Oil, a major driver for emerging markets such as Russia, Brazil & Mexico has been losing ground on fears of deep recession.

Market view: Expect markets to remain volatile & range bound till credit becomes cheaper. Economic stimulus by the government would be a major source of upward pressure on the markets & an upside down turnaround of the economy is not expected in a short period of time, hence don’t expect the economic data to show any improvements in the near future; which would cause a major downward pressure on the markets. Volatility should subside in a time frame of (6 – 12 months). In-case the pain increases dollar & yen are expected to appreciate. Long term view: Emerging markets will outperform SPX but more pain may see oil go down further & emerging markets underperform SPX

Structuring (Term: 1 year)

- Deepening crises would be accompanied by falling oil & appreciating US Dollar (a strong indicator of the crises situation). In such a scenario SPX will outperform MSCI EMEA Index (Emerging markets Index).

- Structure: Up & in outperformance call spread (SPX - MSCI EMEA Index), with up & in barrier on US Dollar (at +105%) & a participation P ranging from (120-150%)

- Incase dollar falls (-10% i.e. back to its normal levels) MSCI EMEA Index is expected to outperform SPX. Hence short a down & in outperformance put on (SPX - MSCI EMEA Index), with dollar as a down & in barrier (at -110%)

- Funding call spread through put (barrier’s can be chosen to design a zero cost structure)

- A good time to fund cheap skew since structure is long SPX skew & short MSCI EMEA Index skew

- Structure is long US dollar-SPX correlation & short US dollar-MSCI EMEA correlation

- Considering US dollar against EUR, the structure is long EUR-MSCI EMEA correlation. A lot of banks operating in emerging markets had sold Quanto EUR/GBP calls on MSCI EMEA thus making them Long EUR-MSCI EMEA/ GBP - MSCI EMEA correlation. Given that the above structure is Long EUR-MSCI EMEA correlation, it provides more incentive for the banks to trade it & offset its long correlation exposure.

Friday, December 19, 2008

Saturday, July 5, 2008

Tougher times demand for Tougher Structures

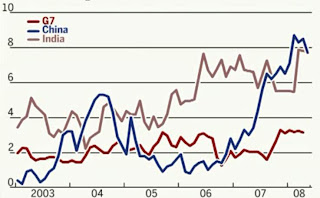

The above figure suggests that Brazil is the only country(in BRIC nations) which has been able to sustain growth in their equity markets during high inflation pressure & world credit crises.

The above figure suggests that Brazil is the only country(in BRIC nations) which has been able to sustain growth in their equity markets during high inflation pressure & world credit crises. The above figure gives PE multiples of the MSCI China, India, APAC indices relative to the MSCI all world index. (P/E multiple is essentially the Price you are willing to pay for a $ earning of the company. Obviously you would expect it to be high if you expect high growth & hence its a reflection of expected growth ). The graph we see is a reflection of expected growth of emerging markets relative to the world markets in the near term. One thing which is apparent from the graph is people have always expected India to grow at a faster rate than China. Would definitely be interesting to plot a PEG( P/E ratio / Growth in EPS ) graph as it gives a measure of expected growth/ Realized growth.

The above figure gives PE multiples of the MSCI China, India, APAC indices relative to the MSCI all world index. (P/E multiple is essentially the Price you are willing to pay for a $ earning of the company. Obviously you would expect it to be high if you expect high growth & hence its a reflection of expected growth ). The graph we see is a reflection of expected growth of emerging markets relative to the world markets in the near term. One thing which is apparent from the graph is people have always expected India to grow at a faster rate than China. Would definitely be interesting to plot a PEG( P/E ratio / Growth in EPS ) graph as it gives a measure of expected growth/ Realized growth. The above graph gives the annual Inflation figures (in CPI %). The devil "CRUDE" is majorly reposnsible for the rising inflation. Since crude has played so much havoc, its worth analyzing the crude economics.

The above graph gives the annual Inflation figures (in CPI %). The devil "CRUDE" is majorly reposnsible for the rising inflation. Since crude has played so much havoc, its worth analyzing the crude economics.Crude's a commodity traded in $. Sources of supply: Middle East Arab Nations, Sources of demand: All of us ! Lets try and justify the rise of crude from $98 per bbl in Jan 08 to the current level of $143 per bbl. Major factors affecting crude prices are as follows.

1. Political disturbances in the middle-east - Not any major ones that I know of in the period Jan 08 - June 08 . Except the current Israel-Iran conflict.

2. FX USD/Investor CCY - since crude is traded in $.

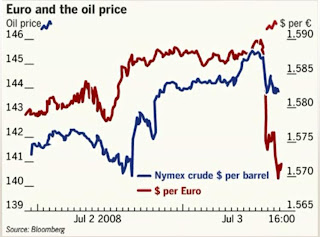

The above figure accentuates the FX/ Crude correlation. Just before the fall Trichet, ECBs chairman announced that it has no further rate cuts in mind & hence dollar strenghtened against EUR & Crude fell.

The above figure accentuates the FX/ Crude correlation. Just before the fall Trichet, ECBs chairman announced that it has no further rate cuts in mind & hence dollar strenghtened against EUR & Crude fell.

$ has depreciated against most of the ccy's like EUR, JPY,GBP (Major crude investors) which has prompted Investors to invest in crude & hence a rise in price.

3. Supply & Demand

Another pressure might be in the fundamentals – how much supply is available, and how much demand there is. In a normal market, an increase in demand for a finite amount of a commodity (which would result in a decrease in inventories) would cause the price to rise. But not so with crude oil: since January 1, 2008, the spot price for crude oil has been rising in spite of an increase in crude oil inventories. See the graph above. (As seen in this graph, as the inventory rose from 295,000 thousand bbls. to 325,000 thousand bbls., the price increased from approximately $90 to $120 per bbl.). From the data in this graph, it is apparent that the normal relation of supply vs. price has not been occurring since January 1, 2008. So the price rise is not due to real demand & most of the positions are speculative ones.

Another pressure might be in the fundamentals – how much supply is available, and how much demand there is. In a normal market, an increase in demand for a finite amount of a commodity (which would result in a decrease in inventories) would cause the price to rise. But not so with crude oil: since January 1, 2008, the spot price for crude oil has been rising in spite of an increase in crude oil inventories. See the graph above. (As seen in this graph, as the inventory rose from 295,000 thousand bbls. to 325,000 thousand bbls., the price increased from approximately $90 to $120 per bbl.). From the data in this graph, it is apparent that the normal relation of supply vs. price has not been occurring since January 1, 2008. So the price rise is not due to real demand & most of the positions are speculative ones.

There's going to be a time when the speculators are going to realize that their love for crude was just an infatuation & they will move on to some other asset class & book in profits on their oil positions - This should see the end of oil bubble BUT given the conditions USD doesnt weaken anymore & US economy rebounds with no major rate cuts, But again bouncing back of US economy so much depends on crude prices......Meanwhile Real-esate has already bottomed out in US so the next move of the speculators is very much predictable.

Structure recommended for the current Scenario: I am not sure of the time when crude prices will start receding to normal levels, Rather I am not sure when a particular asset would give me its best performace in the near term(2yrs) horizon. Structure like Himalayas, Cherry Pickers can prove to be handy in such scenarios.

Basket Construction for such products:

1.Equities: Given the fact that Brazilian Economy has outperformed its peers in tough times & Retail has been a major growth driver for all emerging markets, an equally wghted basket of Indian & Brazilian Retail+FMCG stocks would'nt be a bad pick.

2. Commodities: Crude has the power to outperform any asset class in the near term.

3. US Real estate Index for Long term: Hoping it gives a considerable return after 2 years as a result of US economy bouncing back from the recessionary period.

4. FX (Basket of USDEUR, USDJPY, USDGBP): Has a strong correlation with crude, If FX performs well, crude can turn out to be a waste...

Volatility of commodities has risen up lately. DJAIG Commodity Index vol (6m) has risen to the levels of 21%~22% as compared to previous low levels of 15%~16%. Traditionally it has been equities on which clients have sold or bought vols (as counterparties - generally banks have been able to easily hedge it by buying/selling calls/puts), but with commodties showing significant vol levels, this time Clients might be just interested in playing the big vol game on commodities as well (especially hedge funds). Its a good opportunity for banks as they can charge a better margin since its difficult to hedge volatility exposures on commodities. (To hedge vega, i.e is by buying calls/puts - Broker's the way out, but obviously you have to pay an extra premium & that you can charge from the Client).

Currently commodities have been a part of structures such as Volcaps which dont have high Vega. In Volcaps the asset wt. keeps on rebalancing on the basis of the levels of volatilities reached.

Tuesday, June 3, 2008

Worst of Autocallable II

2.Theta Analysis

The Autocall Theta Analysis provides some very interesting results.

The analysis was done today morning when the Spot was somewhere close to 4% above strike.

Spot has moved by -1.2% today. And the Gamma plus Postfix Values from this analysis on SAN.MC are almost very close to the actual Delta change on the option.

The methodology adopted:

Price Change with SAN on Diff Dates with different spot sets:

A little less importantly: I studied the theta on TEF as well. The delta on TEF behaves very strangely, I'm not sure it is not purely noise as SAN gives the majority of delta and on margin Delta on TEF behaving wierdly

The Autocall Theta Analysis provides some very interesting results.

The analysis was done today morning when the Spot was somewhere close to 4% above strike.

Spot has moved by -1.2% today. And the Gamma plus Postfix Values from this analysis on SAN.MC are almost very close to the actual Delta change on the option.

The methodology adopted:

- A given set of spots was considered for SAN and for TEF. For these spots, the option price was calced for each of the dates from now to the 21st

The Spot sets were taken as

- a) The present Spot on SAN and TEF b) One Percent Bump on SAN c) One Percent Bump on TEF

- a) -2% Bump on SAN and TEF and from there b) One Percent Bump on SAN c) One Percent Bump on TEF

- a) -4% Bump on SAN and TEF and from there b) One Percent Bump on SAN c) One Percent Bump on TEF

- a) -6% Bump on SAN and TEF and from there b) One Percent Bump on SAN c) One Percent Bump on TEF

Point to note is -4% of Spot on TEF behaves most strangely as it is close to strike. The Data might include some noise as at -4% there is no convergence. Unit Deltas were calced but the Dollar delta can easily be calced from fx and notional from Data.

To Confirm, at present spot and at -2% spot, the levels are above autocall strike. At -4% it is just below strike and at -6% it goes below level

Price Change with SAN on Diff Dates with different spot sets:

Price Change with TEF on Diff Dates with different spot sets:

A little less importantly: I studied the theta on TEF as well. The delta on TEF behaves very strangely, I'm not sure it is not purely noise as SAN gives the majority of delta and on margin Delta on TEF behaving wierdly

Monday, June 2, 2008

Worst of Autocallables I

1. Delta Analysis

The methodology adapted was as follows:

The methodology adapted was as follows:

- Take an Autocall with common underlyings ( NESN and NOVN) and expiry in 2011, with a coupon payment and early redemption on worst off performer

- So as to remove extreneous factors, including cross gamma, one of the underlyings was kept constant and the analysis was run on NOVN. Also the Normal structure of autocall product with put was assumed to be without put. This assumption would not make a difference to deltas

- With an intent to simulating the spots going to some percentage of strike and finding price of option, the spots were kept constant and the strikes were adjusted accordingly ( so that the vol params are not affected)

- Two cases are required:

Case 1) The autocalling date has just passed, and the next autocall date is in a year.

Case 2) The autocalling date is in two days

- From the price of the option, we can calculate the deltas and find out how option behaves. The results are as follows:

{kind=link}

Delta Curve wrt Spot

On delta, the second derivative, there is a slight amount of noise, due to which the curve is not perfectly smooth

Conclusion:

Conclusion:

- Delta Values after about 85% of spot start showing a change and increase in case of Autocall with short time to maturity.

- The influence on Postfix deltas to do ( assuming products do not autocall ) is that

A) In case of one underlying below 80%, There should be negl delta to do postfix, assuming it does not autocall.

B) In case of one of the underlyings being between 85-100% there could be between a reasonable and significant amount of delta to unwind.

C) Assuming we are short the autocall, and that the product does not early redeem. We always have to sell stocks, and not sometimes buy as the Euclid Model was showing sometime back. - Cross Gamma effects, in case both Stocks are below the 100% limit, would not be significant (except that the net delta would be distributed accordingly between the two stocks). The Graphs on the worst off stock would look similar to above curves in this case also, though it might change between the two stocks at some time.

Subscribe to:

Posts (Atom)